Walking into a credit union feels much like walking into a bank. Both offer similar services such as checking accounts, mortgages and loans. Both have tellers, ATMs and online access.

But behind the scenes, their operations are fundamentally different.

Banks are owned by stockholders and their operations are designed to make a profit for those owners.

Members own credit unions. Anyone who has any type of an account at a credit union is part-owner in the institution and has a vote in who sits on the board — or can run for membership on the board.

Another key difference is the way the two institutions generate capital, Wally Murray, president and CEO at Greater Nevada Credit Union (GNCU), explained.

Banks generate capital by selling stocks.

“By law (credit unions) are not-for-profit,” Murray told the NNBW in a recent phone interview. “Our goal is not to generate profits, it’s to find ways to benefit the members. The only capital we generate is from earnings.”

The credit unions hang on to enough of those earnings to maintain a healthy financial institution and pass the rest on to their members through reduced fees and other benefits.

Danny DeLaRosa, market vice president Nevada for United Federal Credit Union (UFCU), concurred.

“Credit Unions, like banks, “can do mortgages, business loans, investments — along with taking deposits and loans,” DeLaRosa said in an email response to questions from the NNBW. “The biggest difference, though, is that as a not for profit we can be more competitive in our dividend rates and in our lending rates. We also save our members money with free products and services like our online banking and mobile app or free checking accounts.”

Members also benefit from a nationwide alliance of credit unions, which means members in a geographically limited credit union have ATM access nationwide.

“Our ATM network is part of well over 30,000 across the nation that members can use for free,” Murray said.

Each credit union has requirements for membership, such as participating in employee groups, associations, religious or fraternal affiliations and residential areas. But those criteria have greatly expanded, opening credit union membership to more people.

“Most people think you have to be part of a certain company to join a credit union,” DeLaRosa said. “While that may have been true in the past, recent changes have opened up membership to more people in our communities. For United, if you live or work in Northern Nevada, you can take advantage of the great benefits our credit union has to offer.”

UFCU in Northern Nevada has nine full-service locations and one high school branch. It’s also part of a larger, national institution that began in 1949 in Michigan by employees of the Whirlpool manufacturing plant. Nationally, UFCU has 30 locations in six states serving 150,000 members with $2 billion in assets. Membership requirements vary by state.

GNCU, which is headquartered in Carson City, also began in 1949 and was originally chartered to serve state employees.

Today, GNCU has 64,000 members in Northern Nevada doing businesses in 15 branches with $825 million in assets. Today, anyone living or working in Nevada can join.

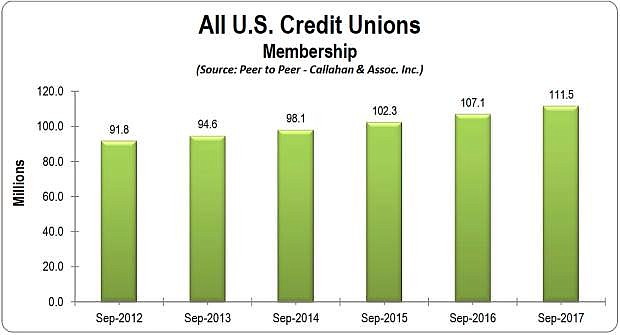

Changes in credit union memberships and trends in banking have been good for credit unions.

“We’ve been growing for the last several years and growing significantly,” Murray said.

According to DeLaRosa, the National Credit Union Administration reported in September that nationally, median loan growth in federally insured credit unions was 4.4 percent in the second quarter this year. Median asset growth was 3.9 percent, and the median rate of growth in deposits and shares was 4.1 percent.

Credit unions have one big disadvantage.

“Banks typically feel threatened by credit unions,” Murray said. “Laws have popped up that limit our ability to serve.”

One such law, passed 20 years ago with pressure from banks, caps the amount of business lending that a credit union can do, Murray said. Such restrictions are not only detrimental to credit unions, but also to their communities.

“It was particularly detrimental during the recession when small businesses were unable to get loans from banks,” he said. “Credit unions couldn’t help.”

With a membership base, credit unions are naturally more connected to their communities.

“Our economy is rebounding from the recession and consumer confidence is returning,” DeLaRosa said. “During the recession, United Federal Credit Union continued to grow and expand. Our communities knew that we were there for them even during difficult times. Helping businesses make it through difficult times and assisting families to get back on their feet have set credit unions apart. Our community values the relationship banking and knowing that in good times and in not so good times their credit union is there for them.”

Comments

Use the comment form below to begin a discussion about this content.

Sign in to comment