The National Association of Realtors (NAR) recently held the Sustainable Homeownership Conference at the University of California, Berkeley, where a group of experts discussed potential ways to reverse the decline in homeownership. This is a topic of recent interest in Reno-Sparks, and much is being done to work on the issue of housing affordability. During the meeting, the five main reasons why would-be buyers are locked out of the housing market were discussed. The reasons are below, and I’ll provide my insight into them from a local perspective.

Post-foreclosure stress disorder

The Great Recession caused long-lasting psychological changes in the financial decision-making for the estimated 9 million homeowners who lost their homes to foreclosure, and the millions who lost their jobs. While I am not a psychologist, I can tell you that the effects were far-reaching, and not to be under estimated. For those who lost their jobs and then subsequently their homes, they now may have recovered financially on paper from the loss and be ready to acquire a home. However, emotional loss has not been forgotten. They are approaching homeownership cautiously, yet not wanting to subject themselves to the trauma experienced from 2005 to 2011. The recession also impacted the children of those families who are now future homeowners. The good news is that according to the National Association of Realtors Profile of Homebuyers and Sellers 2016, 82 percent of reported buyers continue to see purchasing a home as a good financial investment.

Mortgage availability

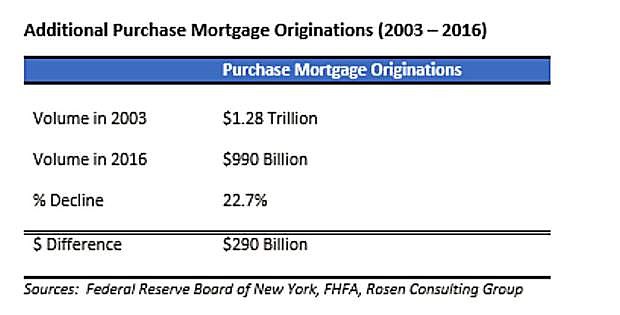

Credit standards have not normalized since the recession, and borrowers with good-to-excellent credit scores are not getting approved at the rate they were in 2003. There’s a saying in the market: “Money is readily available to borrow to those who don’t need it.” Lending has decreased as banks have withheld loan approvals from many households, even those with excellent credit scores. Credit standards have loosened slightly since the end of the Great Recession, and mortgage lending has slowly improved. According to Rosen Consulting Group, who prepared a study for the National Association of Realtors in June 2017, the total purchase lending declined by 22.7 percent between 2003 and 2016, falling by approximately $290 billion to slightly less than $1 trillion in home purchase mortgage originations.

Growing burden of student loan debt

Repaying student loan debt is making it difficult for young households to save for a down payment and qualify for a mortgage. According to the National Association of Realtors Profile of Home Buyers and Sellers 2016, 26 percent of the first-time homebuyers responding said saving for a down payment was the most difficult step in the process. Of that share, 55 percent said student loan debt delayed them in saving for a home.

Locally debt, along with rising rents, compound the difficulty experienced by potential first-time homebuyers to realistically save the dollars necessary to accumulate funds for a down payment.

Single-family housing affordability

Lack of inventory, high home prices and high rents are causing decaying affordability conditions in many markets. Although it may feel as though Reno, Sparks and Washoe County aren’t the only areas impacted by this, increasing home prices and rents along with low inventory are a national issue. The chart with this story displays how Reno home price increases compare to other Metropolitan Statistical Areas.

Single-family housing supply shortages

Nationally, as of April 2017, the inventory of existing for-sale single family homes increased during the past five months to 1.7 million, yet inventory is down by 8.6 percent from a year earlier, according to NAR. Moreover, the supply of homes for sale in April 2017 was down by 1.6 million compared with the pre-recession peak in 2007. Months of supply, which measures the number of months it would take for the current inventory of homes on the market to sell given the current pace of sales, fell steadily during the last three years to a 12-year low of 4.3 months in 2016, from 5.2 months in 2014.

The current months of supply was dramatically lower than the post-recession peak of 10 months in 2008, and since 1983 is the lowest level of months of supply, besides 2004, when this measure was also at 4.3 months. If the inventory of existing single family homes does not improve, home prices will continue to increase, reaching record-highs or near-peak levels in many markets, depressing homeownership growth. This along with an inadequate level of homebuilding has led to a cumulative deficit of nearly 3.7 million new homes over the last eight years.

In Washoe County (excluding Incline Village), units sold compared to new listings historically follows a seasonal pattern of highs and lows in units sold and new listing inventory. Prior to 2017, new listings were between 28 percent and 41 percent ahead of units sold for the months January-June. For the first six months of 2017, the average is 21 percent.

In conclusion, we are not unique. This problem exists to a greater or lesser degree across the country. There is no “silver bullet” that can quickly mitigate any of the hurdles to home ownership that we are experiencing today. There have not been enough new housing units built to meet demand for several years. Builders are beginning to build once again; however, at the current rate of construction along with prices mostly above the area median price, it will be several years before our inventory comes into balance.

By John Graham is the 2017 RSAR President and a Realtor with RE/MAX Premier Properties.

Comments

Use the comment form below to begin a discussion about this content.

Sign in to comment